CUSTODIAL VS. NONCUSTODIAL PARENTS

Glen and Gail Newsome have divorced this year. Their 14-year-old child, Dawn, lives with Gail for a majority of the year and with Glen from mid-June

through August. Glen and Gail each provide half of Dawn’s support. The divorce decree specifies that Glen can claim Dawn as a dependent in odd-numbered

years, and Gail can claim Dawn as a dependent in even-numbered years. In the odd-numbered years, Gail signs Form 8332 to release claiming Dawn as a

dependent to Glen.

Gail can file as head of household (HOH) because she paid more than half the cost of maintaining her home, which is also Dawn’s home for the majority of

the year. Even though Gail released her claim to the child as a dependent to Glen, it does not affect her

ability to claim HOH status.

Regardless of whether the custodial parent releases the exemption, both parents are eligible for itemized medical expenses and tax-free health savings account

(HSA) distributions.

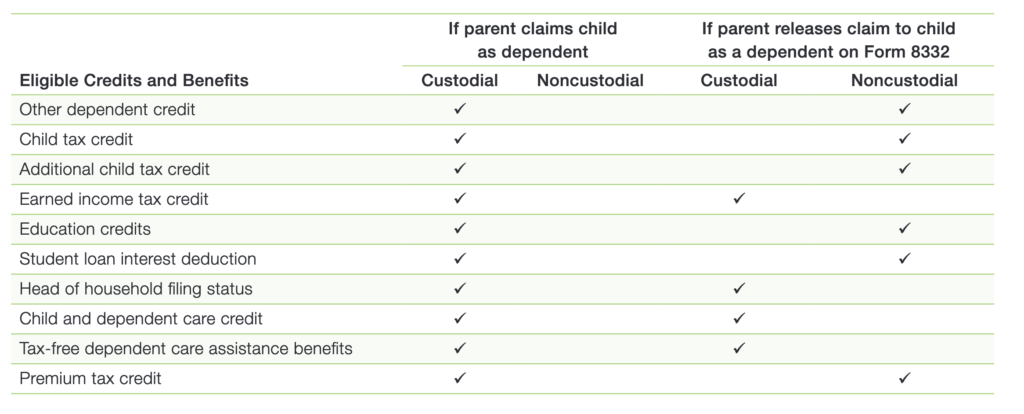

The chart below summarizes which benefit each parent receives when the custodial parent releases the dependency to the noncustodial parent. If the custodial

parent did not release the dependency exemption, the custodial parent would receive all the benefits, and the noncustodial parent wouldn’t receive any.

In addition, the child is the dependent of both parents for purposes of the medical expense deduction rules, regardless of whether the custodial parent

releases the claim to the child as a dependent, if the taxpayers are both of the following:

• Divorced, legally separated under a decree of divorce or separate maintenance, legally separated under a written separation agreement or lived

apart at all times for the last six months of the calendar year.

• Parents of a child who meets the following provisions: (1) receives more than half of their support during the calendar year from their parents; (2) is in the custody of one or both parents for more than half of the calendar year, and (3) qualifies as a qualifying child or qualifying relative of one of the child’s parents (Rev. Proc. 2008-48)

Medical expenses covered under this provision include medical expense reimbursements or deductions, excludable fringe benefits, and distributions from an HSA or Archer MSA.